🎅 🎄🥂🍻🎁🛍

Are you planning any Christmas celebrations with your staff and/or business associates?

Best to refresh your memory on the allowable deductions & FBT rules before the event so you don’t end up with any surprise tax to pay!

🛍🎁🍻🥂🎄🎅

Click here to read it from the horse’s mouth so to speak: https://www.ato.gov.au/General/Fringe-benefits-tax-(FBT)/In-detail/FBT-and-Christmas-parties/

We’ve also pasted the details from the ATO website below:

Fringe benefits tax and Christmas parties

Christmas parties

There is no separate fringe benefits tax (FBT) category for Christmas parties and you may encounter many different circumstances when providing these events to your staff. Fringe benefits provided by you, an associate, or under an arrangement with a third party to any current employees, past and future employees and their associates (spouses and children), may attract FBT.

Implications for taxpaying body

If you are not a tax-exempt organisation and do not use the 50-50 split method for meal entertainment, the following explanations may help you determine whether there are FBT implications arising from a Christmas party.

Exempt property benefits

The costs (such as food and drink) associated with Christmas parties are exempt from FBT if they are provided on a working day on your business premises and consumed by current employees. The property benefit exemption is only available for employees, not associates.

Exempt benefits – minor benefits

The provision of a Christmas party to an employee may be a minor benefit and exempt if the cost of the party is less than $300 per employee and certain conditions are met. The benefit provided to an associate of the employee may also be a minor benefit and exempt if the cost of the party for each associate of an employee is less than $300.The threshold of less than $300 applies to each benefit provided, not to the total value of all associated benefits.

Gifts provided to employees at a Christmas party

The provision of a gift to an employee at Christmas time may be a minor benefit that is an exempt benefit where the value of the gift is less than $300.

Where a Christmas gift is provided to an employee at a Christmas party that is also provided by the employer, the benefits are associated benefits, but each benefit needs to be considered separately to determine if they are less than $300 in value. If both the Christmas party and the gift are less than $300 in value and the other conditions of a minor benefit are met, they will both be exempt benefits.

Tax deductibility of a Christmas party

The cost of providing a Christmas party is income tax deductible only to the extent that it is subject to FBT. Therefore, any costs that are exempt from FBT (that is, exempt minor benefits and exempt property benefits) cannot be claimed as an income tax deduction.

The costs of entertaining clients are not subject to FBT and are not income tax deductible.

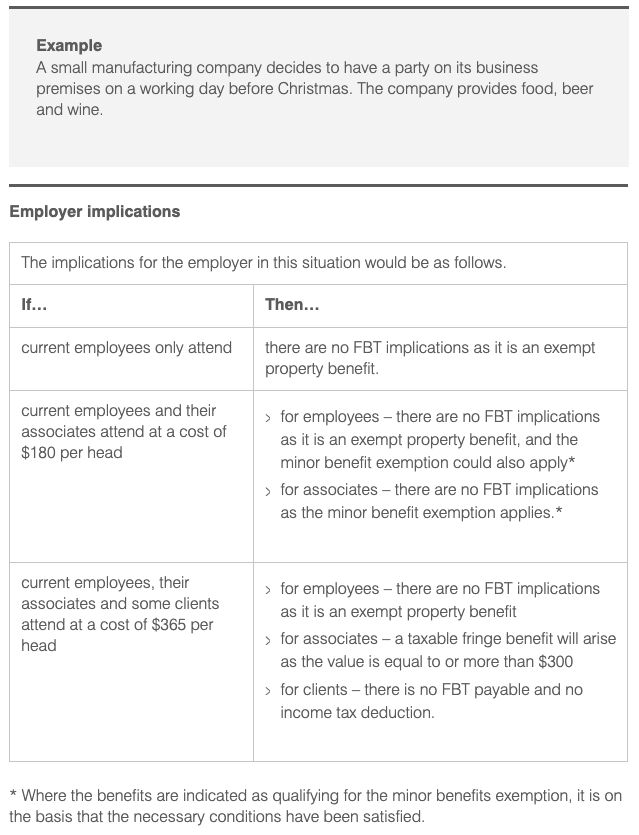

Christmas party held on the business premises

A Christmas party provided to current employees on your business premises or worksite on a working day may be an exempt benefit. The cost of associates attending the Christmas party is not exempt, unless it is a minor benefit.

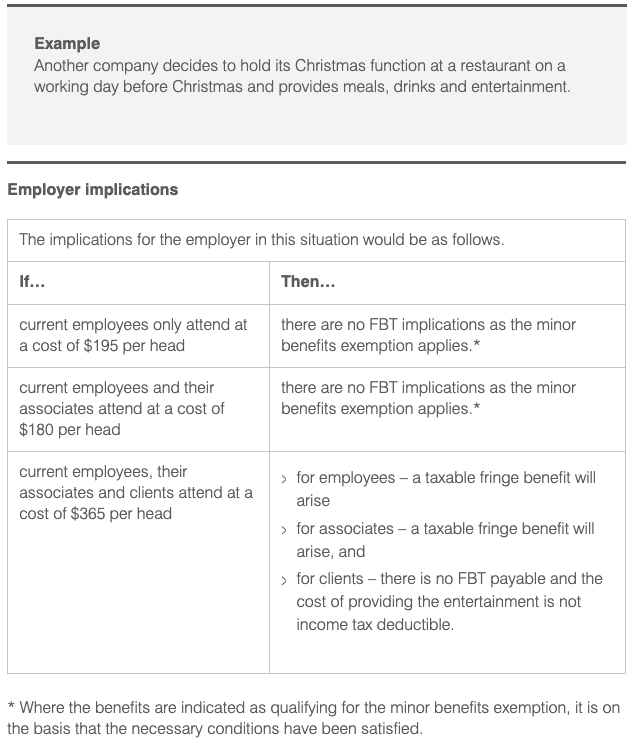

Christmas party held off business premises

The costs associated with Christmas parties held off your business premises (for example, a restaurant) will give rise to a taxable fringe benefit for employees and their associates unless the benefits are exempt minor benefits.